What to Expect if You Are Served with a Lawsuit by Your MCA Lender

If you have defaulted on an MCA, here’s what can generally be expected if a business is served with a lawsuit by an MCA lender (we will assume you signed a personal guarantee):

1. Receipt of a Summons and Complaint: The first step in any lawsuit is the delivery of a summons and complaint. This document outlines the claim that the MCA lender is making against the business owner. The summons and complaint will generally be served to the business owner in person or via certified mail.

2. Response Due: After receiving the summons and complaint, the business owner has a limited period of time (usually around 20 days, but this can vary depending on the jurisdiction) to respond or answer the complaint. If a response is not filed within this period, the court may enter a default judgment against the business.

3. Court Hearing: If the business owner and MCA lender cannot reach a settlement, the case will likely proceed to court. A judge or jury will hear the case and make a determination.

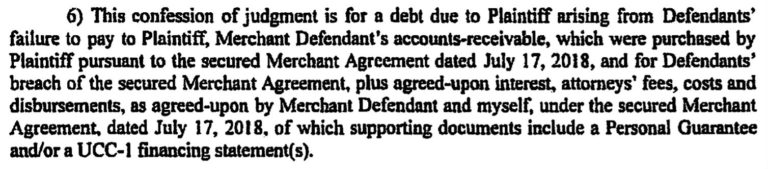

4. Judgment: If the court finds in favor of the MCA lender, it will issue a judgment ordering the business owner to pay a certain amount. This amount will typically include the outstanding balance of the MCA, along with penalties.

5. Interest and Fees: The judgment may also include provisions for the accrual of interest on the unpaid balance, as well as the payment of legal fees incurred by the MCA lender.

6. Collection Activities: If the business owner is unable to pay the judgment, the MCA lender may engage in various collection activities. This can include wage garnishments, liens on property, or repossession of collateral associated with the advance.

Failure to Pay

Depending on the specifics of your contract with the MCA provider and the laws of your jurisdiction, if you fail to pay the judgment or are unable to meet your repayment obligations, the MCA provider may pursue various collection activities. Here are some possibilities:

- Garnishing Wages: In some cases, a court can order that a portion of your wages be withheld and sent directly to the MCA lender to pay off the debt. This is known as wage garnishment. However, this is more typical in consumer debt cases and may not be applicable to businesses.

- Placing Liens on Property: A lien is a legal claim on an asset that allows a lender to seize and sell it if a debt is not paid. If the MCA lender places a lien on your property (such as your business premises or other assets), they could potentially sell the property to recover the debt.

- Repossessing Collateral: If your MCA agreement included any collateral (assets pledged as security for the advance), and you default on your payments, the MCA lender may have the right to repossess and sell these assets to recover the amount owed. This could include business equipment, inventory, or other valuable assets.

Each of these collection activities has legal requirements and protections in place, so it’s crucial to consult with an attorney if you find yourself in this situation. They can help you understand your rights and options and advocate on your behalf.

If You Signed A Personal Guarantee

A personal guarantee blurs the line between your personal finances and your business finances. A personal guarantee is an agreement that holds the business owner (along with cosigners) personally responsible for repaying the business loan or cash advance. It effectively bypasses the protection that business structures like LLCs or corporations usually provide their owners.

If you’ve signed a personal guarantee as part of your MCA agreement, this means that if your business is unable to repay the advance, the MCA lender can come after your personal assets to recoup their money. This can include your personal bank accounts, your car, your home, and other personal assets. In this case, the potential consequences of a lawsuit by an MCA lender are not limited to your business but could impact your personal financial situation as well.

Merchant Cash Advance Lawyers

Legal help can be expensive, and there’s no guarantee that a lawyer will be able to find a “loophole” or solution that absolves you of responsibility. Before your attorney even has a chance to log into their LexisNexis and Westlaw accounts to seek potential legal remedies or loopholes, the MCA creditors may have already drained your business accounts, imposed levies on your credit card processor, and reached out to your clients for direct payments to them.

Protected Assets

It’s also worth noting that some personal assets might be protected from creditors, even if you’ve signed a personal guarantee. These “exempt” assets can vary by state but might include a certain amount of equity in your home, your car up to a certain value, retirement accounts, and other personal property.

Settlement Outside of Court

Settling a debt outside of court, often referred to as out-of-court settlement, is a common practice in the world of debt resolution.

Despite the daunting prospects of lawsuits, judgments, or personal guarantees, it’s important to note that these circumstances do not preclude you from negotiating a settlement with your creditors. With the right approach, you have the potential to settle your debt for a fraction of the original amount owed. By following our systematic approach, you can work towards a resolution, regardless of whether you’re dealing with a judgment, lien, or a personal guarantee.