Merchant Cash Advance Confession of Judgement

I Confess!

When you sign a Merchant Cash Advance Confession of Judgement, you sign away your rights to the legal process.

A Confession of Judgement (Cognovit Note/Warrant of Attorney) is an extraordinary weapon creditors use to remedy loan defaults. It allows Merchant Cash Advance companies and other creditors to enter a judgment against debtors without having to give notice when a complaint is filed in court and without a hearing where a borrower would have the ability to defend themselves.

When a Confession of Judgement clause is used in a note and signed by a debtor, then the debtor obligor will have agreed to waive their rights to a notice and hearing prior to judgment if they default on payments. Creditors do not have to litigate. They file a complaint without alerting the debtor, most often electronically, and get a judgment in their favor. This is what gives creditors the incredible speed in their collection process and why it is astonishing to the debtor.

The judgment can act as a lien on a property and receivables. It is often embodied as a clause in a judgment note with the debtor having no clue of its sweeping power. Even if the borrower is not at fault, there is no defense because there is no judicial review and the lender does not have to present proof.

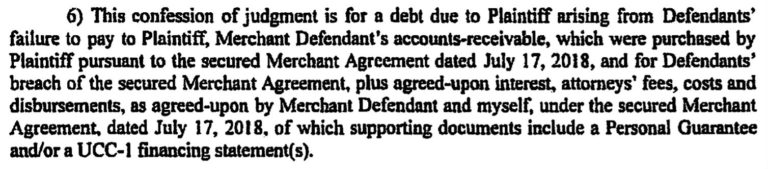

Confession of Judgements can only be used in a commercial setting and was banned for consumer loan use in 1985 by federal regulators. Some states may not recognize a Confession of Judgements but New York does, and that is where most complaints get filed and judgments granted.

Although some states will not recognize confessions, all states recognize judgments from other states. A Merchant Cash Advance company can quickly get a rubber-stamped judgment based on a confession in New York and then start seizing assets from borrowers with no prior notice in any other state. Before the use of confessions, it could take lenders months or years to get a judgment, and they stood little chance of collecting the entire amount of the note. In 2012 the first confession was filed in court by a merchant cash advance company making it possible for a lender to not only have a far better chance of collecting the full amount but also profiting by adding extra fees. Since then there have been over 25,000 judgments granted to MCA companies in New York totaling over $1.5 billion.

Three Rubber Stamps and Judgment!

To win a judgment MCA companies do not need to appear in court. They file electronically and, for example, at the Orange County Clerk’s office in New York, proposed judgments are printed out by a clerk, and each one gets hit by three rubber stamps making them official. There a few other counties in upstate New York doing precisely the same thing.

Clerks process confession filings regardless of any abuses they might contain. A clerk will look at the affidavit sent by MCA lawyers that explains the default and confession, accepts it as fact, and then enter a judgment against the borrower.

Seizure

With a judgment in hand, MCA companies then seize not only borrowers business accounts, but they also seize personal accounts. This is all done without warning and banks do not alert customers before freezing accounts. Confessions allow MCA companies to pounce on debtors with the element of surprise.

Bottom Line

The Confession of Judgement is a legal tool that allows MCA companies to seize assets quickly and efficiently without any prior notice to the borrower. This makes it an extraordinary weapon in the arsenal of creditors.

No Use for Usury - Three Magic Words

There are no federal regulations for MCA companies. This type of lending was created to sidestep any state licensing requirements and usury laws. Lawyers changed the word loan to Merchant Cash Advance defining it as advanced money against future receivables. Those three magic words - Merchant Cash Advance - have conjured up massive profits for aggressive lenders and consumer protection laws are no help to borrowers because they are a business and not a consumer.

The 9 Steps of Confessions of Judgment

1. The Small Business

Requests a loan from a Merchant Cash Advance Company.

2. A Confession is Signed

Small business owner signs contract which includes a confession of judgment

3. MCA Lender

Advances cash to small business owner

4. Default & Dispute

A payment is missed or the borrower blocks cash transfer to the MCA lender.

5. Judgement Day

The MCA lender files a confession of judgment and clerk, rubber-stamps it. It's called "Judgment by Confession."

6. Enter the Marshals

Marshals present demands on the borrower's bank freezing the accounts.

8. The Bank Capitulates

The borrower's bank sends money to MCA lender.

9. MCA Lender Wins Without a Fight

The MCA lender keeps what it claims it is owed along with large fees and interest. This is all done without the borrower knowing.

The above workflow sounds bad but it is only the beginning of the trouble a small business will face when aggressive lenders go after them.